Synopsis: Public sector banks in India have significantly reduced non-performing assets (NPAs) across major lending sectors between March 2021 and March 2025. Industry and MSME loans recorded the biggest improvement, while retail loans continued to maintain the lowest default levels.

PSB NPAs Fall Sharply Across Key Lending Sectors

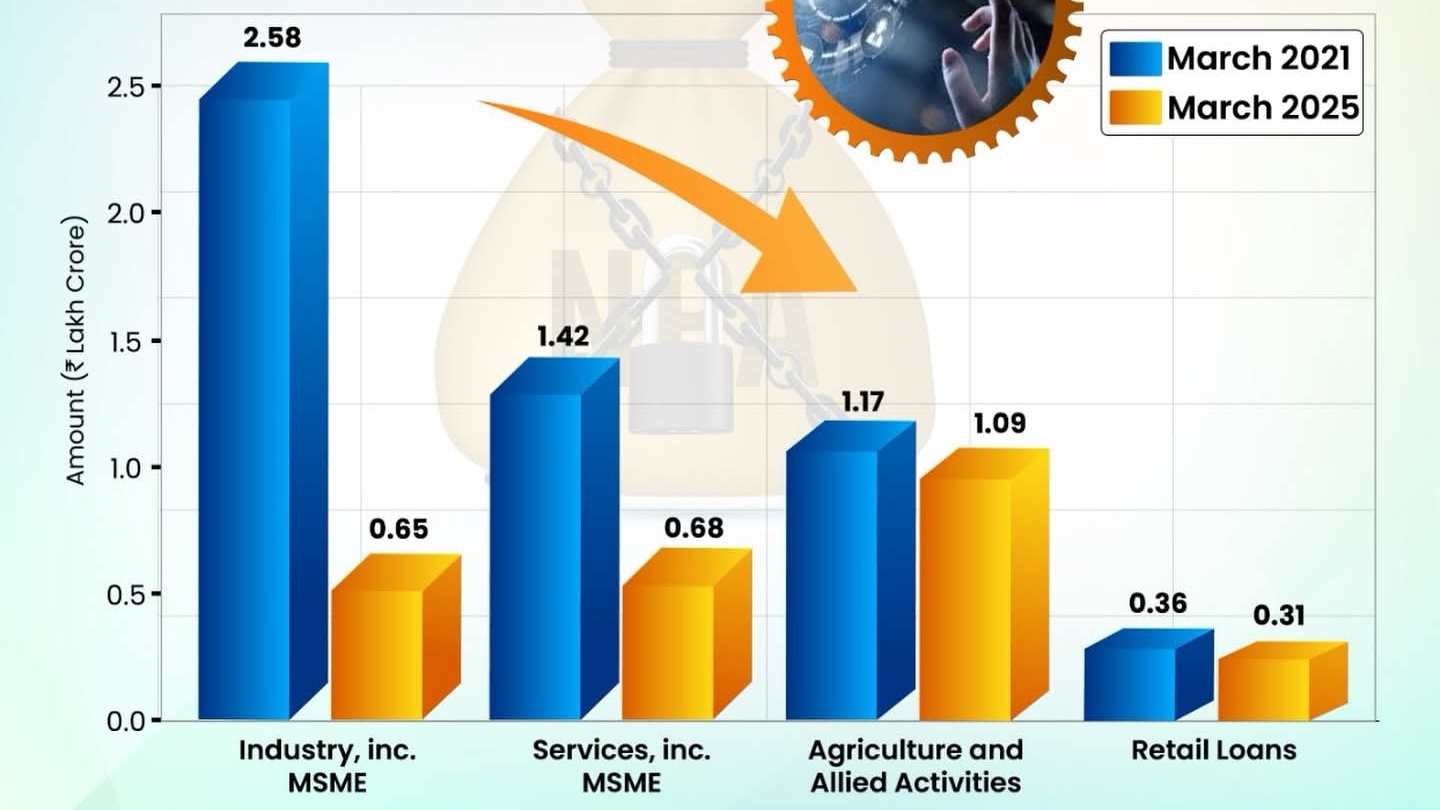

India’s public sector banks (PSBs) have achieved a major reduction in non-performing assets across key sectors of the economy. According to data released by the Department of Financial Services based on figures from the Reserve Bank of India, gross NPAs declined significantly between March 2021 and March 2025.

The improvement reflects stronger credit discipline, better monitoring of loan accounts, and improved recovery mechanisms adopted by banks over the past few years.

Industry and MSME Loans See the Largest Decline

The most notable improvement has been observed in loans provided to industry, including micro, small and medium enterprises (MSMEs).

Gross NPAs in this sector fell sharply from Rs. 2.58 lakh crore in March 2021 to Rs. 0.65 lakh crore in March 2025. This represents a reduction of nearly 75 percent within four years.

Banks strengthened credit appraisal systems, monitoring frameworks, and restructuring support for MSMEs during this period. Government initiatives and improved economic activity also supported borrowers in repaying their loans.

Service Sector NPAs Also Show Strong Improvement

Loans given to the services sector, including MSME-related services, also recorded a significant decline in NPAs.

Gross NPAs in the sector dropped from Rs. 1.42 lakh crore in March 2021 to Rs. 0.68 lakh crore in March 2025.

The services sector had experienced financial stress during the pandemic period. However, recovery in tourism, hospitality, logistics, and digital services has helped improve the repayment capacity of borrowers.

Agriculture Segment Shows Gradual Improvement

Agriculture and allied activities continue to remain an important lending segment for banks.

Gross NPAs in agricultural loans declined moderately from Rs. 1.17 lakh crore in March 2021 to Rs. 1.09 lakh crore in March 2025.

Although the improvement is smaller compared to other sectors, stable rural income and improved loan monitoring systems have helped control stress in agricultural lending.

Retail Loans Continue to Maintain Low NPA Levels

Retail lending continues to remain one of the safest segments for banks.

Gross NPAs in retail loans declined slightly from Rs. 0.36 lakh crore in March 2021 to Rs. 0.31 lakh crore in March 2025.

Banks have increasingly focused on retail lending due to its diversified borrower base, better credit scoring systems, and relatively lower default risk.

Improved Credit Discipline Strengthens Banking System

The steady reduction in NPAs across sectors indicates stronger credit discipline within the banking system.

Banks have enhanced loan monitoring through digital tools, implemented stricter underwriting standards, and strengthened recovery mechanisms. Regulatory reforms and improved risk management practices have also contributed to healthier bank balance sheets.

With NPAs declining steadily, public sector banks are now better positioned to expand lending, support economic growth, and finance new investments across sectors.

📌 Key Takeaway

Public sector banks have significantly reduced NPAs between 2021 and 2025, with the biggest improvement seen in industry and MSME loans. Retail lending remains the safest segment, strengthening the overall stability of India’s banking system.